Please Note: The process and standards described below generally apply to deals underwritten by Percent. We collaborate with numerous third-party underwriters who syndicate deals on our platform. While we aim to ensure these underwriters are a fit for the Percent platform, their practices, and processes related to risk management and underwriting may slightly differ. This diversity enriches our platform with a wide range of opportunities, reflecting our commitment to providing our investors with access to a broad spectrum of private credit deals.

At Percent, we prioritize managing risk and commit to transparency about the risks encountered in private credit investing. On every part of our site — from deal pages to posts like this one — we remain honest and open about the risks faced by investors on our platform.

We encourage investors to consider this information and inquire about how Percent mitigates these risks. This post attempts to share a detailed outline of exactly how our team mitigates and manages risk.

Components of Risk

We believe that risk must be understood on a holistic basis, taking into account all factors affecting investment performance across an entire portfolio. Yet, for the purpose of explaining our risk mitigation procedures, it is easier to group risks for the sake of illustration.

We divide risks into two categories: asset performance risk and counterparty risk. The former relates to when the underlying assets contributing to the repayment of an obligation do not perform as expected, on either an individual or portfolio-wide basis. The latter deals with the risk that the performance of a note becomes decoupled from the underlying assets due to the actions (or inactions) of a transaction party.

Whichever category of risks we are referring to, and though the details may change deal-by-deal, the fundamental approach to risk management usually changes little.

Asset Performance Risk

For most investors, asset performance risk is the easier category to grasp and measure. When buying real estate, for instance, most people intuitively understand that their return depends on the ability of that property to generate cash flows, generally from rent or sale proceeds. Similarly, an asset-backed bond depends on its collateral pool to generate returns.

Many notes offered on Percent’s platform finance the portfolios of specialty finance lenders and are typically backed by the private credit assets they originate. These could include loans, leases, cash advances, receivables, royalties, and more. These assets generate cash flows that can be predicted with some level of accuracy, but not with certainty and not without risk.

Nonetheless, the first step to mitigating asset performance risk is examining the payoff characteristics of the underlying assets. Relevant questions include:

- How frequently do the underlying assets pay?

- Are the assets amortizing or do they repay principal only at maturity?

- How long are repayment periods?

- What proportion of the assets will likely experience collection issues (delinquencies and defaults)?

- Are the assets secured by some kind of collateral, and if so, what is the marketability of that collateral?

- What measures can a borrower or servicer take to mitigate losses on a defaulted asset? And of a given defaulted amount, what is the expected recovery, if one can be ascertained?

- How high is the concentration among the underlying assets in the portfolio with respect to obligor, geographic, or industry concentrations?

- Are the assets denominated in a currency different from that of the notes sold to investors?

For borrowers that are specialty finance companies, an underwriter reviews prospective borrowers’ loan books to answer those questions. Should the underwriter, which may be Percent or a third-party, proceed with that borrower, the underwriter makes information available to investors through offering materials, and Percent provides updates via Surveillance Reports which our internal underwriting team prepares.

Despite best efforts to project asset performance, there will inevitably be some variability. As investors in many notes typically only have recourse, directly or indirectly, to the underlying assets, should cash flows from those assets come in lighter than expected, interest and principal repayment to investors could be impaired.

Asset Performance Risk Mitigants

To mitigate this risk, Percent often requires that borrowers which are specialty finance companies absorb losses on their assets up to a predetermined point. This provides a cushion called “overcollateralization.” Overcollateralization is essentially the value of assets in a portfolio that is in excess of the amount required to fully collateralize a note’s principal value. Historically, this overcollateralization of notes offered on the Percent platform has varied between 0% and 50% of a note program’s portfolio value.

For notes secured by portfolios of assets, underwriters arrive at an appropriate overcollateralization based on the projected default rate of the underlying assets. Other factors, including the presence of any foreign currency risk, concentration risk, delinquency rates, and potential recovery rates on defaulted assets, are also considered. For senior notes, underwriters typically aim to have an overcollateralization that is some multiple of the projected default rate over the life of the note, which we refer to as the “Life Default Rate.”

To illustrate the protection provided by this overcollateralization, suppose a note is collateralized by assets with a 5% default rate. If that note has 20% overcollateralization, the protection would amount to 4x the historical default rate. In this example, even if defaults were to come in at twice their historical level, for example, there would still be ample cushion of principal balance over the note provided by the excess collateral.

Often, overcollateralization tests, or borrowing base tests, are incorporated into the transaction structure. These tests check for sufficient collateral on an ongoing basis. At the close of each note, a borrower is required to provide sufficient collateral to cover both the note amount and any overcollateralization. The overcollateralization tests then check that the collateral continues to stay above some minimum threshold on an ongoing basis (generally either on a daily, weekly, or monthly basis).

The overcollateralization just described is one form of ”credit enhancement,” so named because it improves the credit quality of a note. Other forms of credit enhancement may include cash reserves, guarantees, and credit insurance. Any credit enhancements present in an investment are crucial factors in understanding its risk and, as a result, they are mentioned on our deal pages for investors’ benefit.

However, there are other credit enhancements common to specialty finance notes that are easily overlooked. As an example, in general, the underlying assets backing the notes yield a return higher than what is due to the noteholders. This difference is called “excess spread” and provides yet another cushion to absorb losses. Excess spread is often classified as a “soft credit enhancement” since the spread in any one period is usually released to the borrower before the note matures.

For example, imagine two notes yielding 10%, one backed by assets earning 12% and another by assets yielding 22%. The excess spread is 2% and 12% respectively, and in either case that excess can be used to make up for losses from defaults. It’s worth noting the support provided in the second note is far greater than in the first note. Excess spread is especially crucial for high-yielding asset classes like emerging market consumer credit and merchant cash advances.

Hedging contracts such as currency forwards or option contracts may be added as another credit enhancement mechanism for note programs exposed to foreign currency risk to minimize the mismatch in the currency movement between the assets and the note.

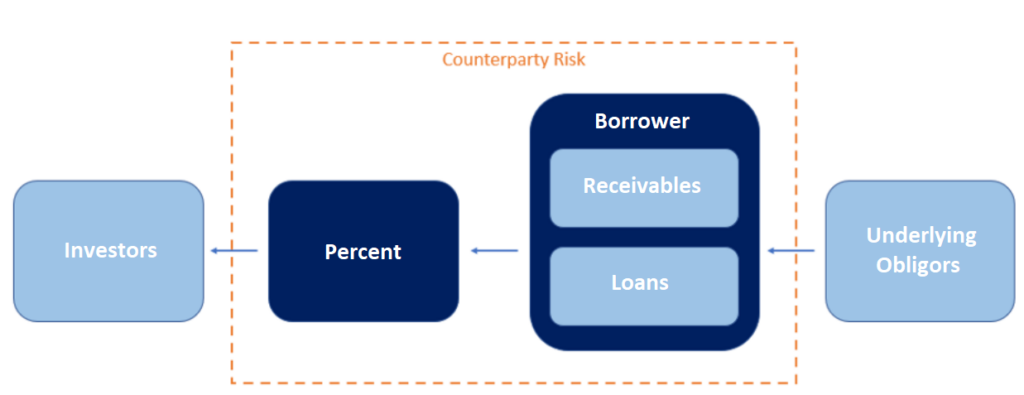

Counterparty Risk

While asset performance risk is the more obvious of the two groups of risks we outlined earlier, counterparty risk shouldn’t be ignored. Counterparty risk refers to the risk of an entity involved in a financial contract not honoring its obligations. This could be due to the financial duress or bankruptcy of that entity, but counterparty risk could also arise from operational failure, fraudulent activities, or gross misconduct by transaction parties.

Counterparty risk is especially relevant in private credit because the sector is more opaque. Whereas most public market transactions are executed through well-known, highly-regulated exchanges and clearinghouses, this is not so in private credit. In private markets, transactions are executed directly between two or more parties, often unregulated and with less public information about them. This means the financial health and operational strength of counterparties matters a great deal more than in public market transactions.

Usually, the two most important counterparties involved in the speciality finance notes offered on the Percent platform are our borrowers and Percent itself.

Borrower Counterparty Risk

The first step to mitigating counterparty risk is understanding the role of the counterparty and assessing the potential for their financial or operational failure. Unless otherwise noted, borrowers and other counterparties go through a due diligence process to uncover and assess these risks. Indeed, quite often, the volume of questions that pertain to counterparty risks exceed those related to the underlying assets themselves.

Our due diligence process reviews prospective key counterparties’ operational and financial capacity, the technology they employ, and various other internal and external risk factors. For specialty finance company borrowers, Percent’s usual counterparty risk mitigation process also includes an operations review of the borrower. An operations review typically features a demonstration of a borrower’s technology platform and also covers staffing, portfolio monitoring, and underwriting and servicing practices. Once again, these initial steps are merely meant to understand the risk of working with a particular party. We also attempt to understand the consequences of an operational or financial failure of a borrower and how to mitigate such consequences.

In addition to our due diligence, we put new borrowers through an internal committee process where several internal experts in capital markets and credit risk share their thoughts on these potential borrowers. As needed, we also leverage outside advisors, legal counsel, and verification agents to provide further perspectives on a particular counterparty or asset class. Whereas many credit committees focus overwhelmingly on financial health or asset performance, we believe a broader scrutiny is particularly important in private credit.

Finally, our agreements with borrowers often provide various legal protections to investors. As an example, borrowers typically represent that they are in good legal standing and that our agreements with them are not in violation of other contracts or regulations that might encumber them. For specialty finance programs, they also represent that they have proper title to the assets they are selling the participation in to Percent.

Specialty finance borrowers also attest that no other entities have a claim to such assets, except in the case of subordinated notes where a specific senior claim is identified and disclosed in the documents. Some of these representations can be verified by background checks that include lien searches, incorporation checks, and more. However, for some of these representations, Percent relies on the truthfulness of the borrower. Breach of these representations allows for the cancellation of a transaction by requiring that the client repurchase the assets they sold. The proceeds from this repurchase would then be paid to noteholders.

Percent may not be able to verify the veracity of each claim or representation made by the borrower. Therefore, despite all efforts to only offer deals with exceptional quality and integrity, there might be rare instances when a borrower may misstate facts or otherwise engage in fraudulent behavior. While not necessarily frequent, we have all heard stories of fraud in the world of finance or outside of it. On the Percent platform too, one of the three defaults that we have encountered to date has been due to fraud. As of the publication date of this blog, Percent is actively litigating the people involved and is hopeful of a fruitful resolution in that case. Percent has taken additional steps to mitigate such risk, such as rolling out collateral verification through a third party, but those steps would only go so far, and the risk of fraud is never fully eliminated.

For specialty finance programs backed by collateral, if a counterparty risk were to materialize, either from an operational oversight, an information security breach, fraud, borrower bankruptcy, or otherwise, it is worth noting that noteholders’ investment would still be backed by the cash flows from the remaining underlying assets, whether they are receivables, term loans, cash advances, and so on. To the extent feasible, Percent would manage the recovery process on behalf of investors in such an unforeseen scenario.

Percent Counterparty Risk

Just as we diligence key prospective borrowers, we perform a similar exercise on ourselves and, in the process, have developed a robust risk management framework to address potential issues.

Not only do we use our committee process to scrutinize potential borrowers or underwriters, we also use them as a forum to discuss potential operational issues that could arise on our end during the life of a transaction. This is especially pertinent to offerings with certain deal features, like embedded call options, more complex cash control arrangements, or transactions that involve a borrower domiciled in a foreign country.

In the unforeseen event that Percent ceases its operations, investors on our platform are protected. Percent employs a backup manager that is responsible for continuing to service note programs in the event Percent is unable. This backup manager would wind down the note programs then outstanding by remitting funds collected from the collateral to investors. Also, investors’ uninvested funds are deposited in an FDIC insured bank account and are not commingled with Percent’s operational bank accounts. The separation of these funds is reviewed by external accountants.

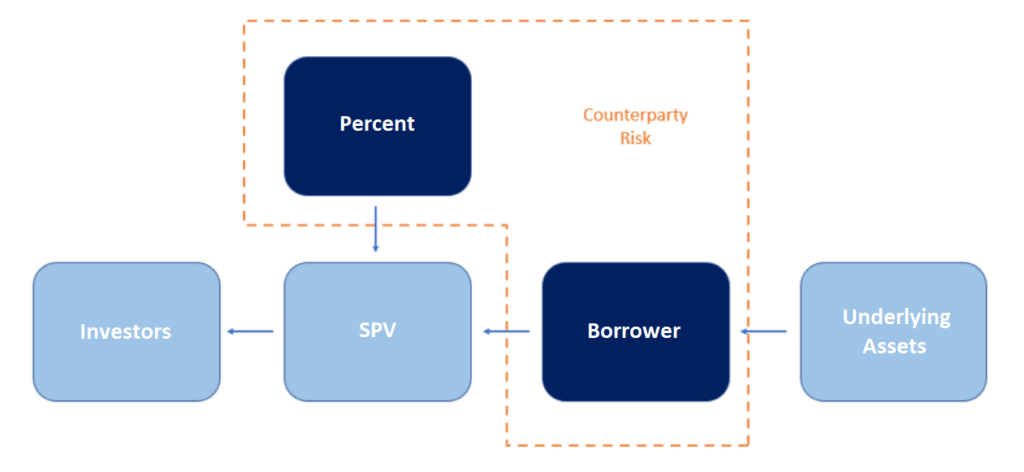

Investors’ funds invested in current opportunities, yet to mature at the time of a hypothetical insolvency, would also be protected. This is done through our use of industry-standard special purpose vehicles (SPVs) that segregate the assets of the note issuer (the SPV) from any of Percent’s assets and liabilities.

To be clear, when you purchase a note on the Percent platform, you are typically not looking to lend to Percent, so we strive to make sure your investment is insulated from any counterparty risks arising from Percent itself.

What are SPVs and How Do They Protect You?

SPVs are separate legal entities, typically formed through limited partnerships (LPs) or limited liability corporations (LLCs), that are used to separate an entity’s assets and liabilities from those of other entities that might otherwise be related. SPVs create a “bankruptcy-remote” entity whose creditors and other interested parties are substantially less exposed to the financial, operational and legal health of any other entity, at least from a bankruptcy perspective. For instance, even if a parent company goes bankrupt, an SPV it owns equity in can continue to pay its creditors, provided proper precautions were taken to make it truly bankruptcy-remote.

The use of SPVs in structured finance and other financial market applications has been around for decades. This is because investors value the protection that they offer in preventing hidden risks from materializing because, for example, a creditor somewhere else in an organization was able to lay claim to collateral they thought was meant to secure their claim specifically.

In its specialty finance investment offerings that Percent makes available to investors on its platform, a bankruptcy-remote SPV is usually used. These SPVs typically only have a single set of assets and liabilities. The assets are participation interests in the invoices, royalty agreements, loans, and other financial assets that back the notes. The liabilities are the Percent notes issued to investors. We believe this structure is more investor-friendly than lending to the specialty finance companies directly because it reduces dependence on the borrower and the impact of the health of the borrower deteriorating for some unforeseeable reason. We also believe that with scale, setting up SPVs can be done in a very cost-efficient manner, reducing costs that would otherwise be borne by the investor, the borrower, or Percent.

Recall that we explained that counterparty risk could cause the performance of a note to become decoupled from the underlying assets due a transaction party not honoring a commitment, either out of intentional breach of contract or operational shortfall. We hope it is clear now why using an SPV helps reduce counterparty risk. This applies to the counterparty risk introduced by Percent or our borrowers or underwriters.

By understanding the different components of risk and how they work in conjunction with Percent’s investments and operations, you should now have a clearer understanding of the risks involved in private credit investing and how Percent and other underwriters typically mitigate those risks. At Percent, we believe that making private credit less opaque opens up the asset class to investors who would otherwise be unfamiliar or uncomfortable exploring this alternative asset class.